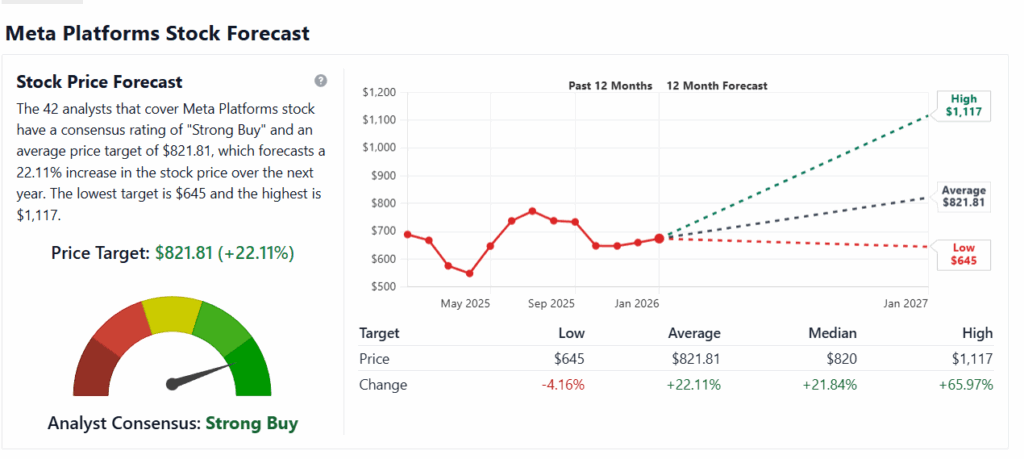

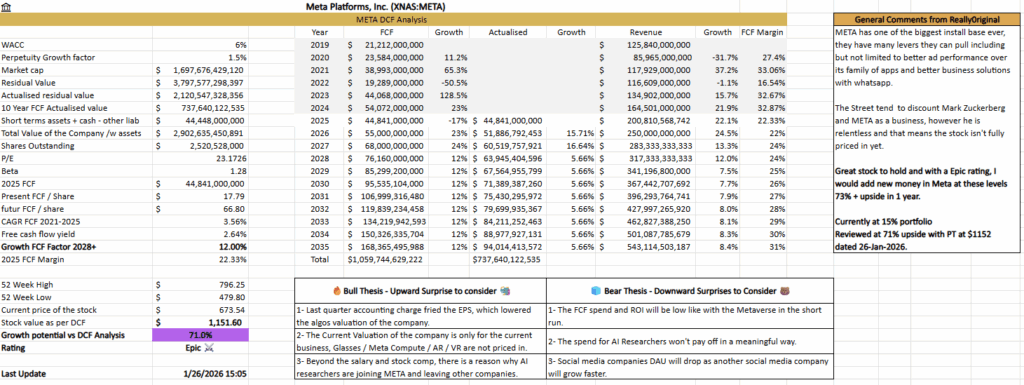

META – Epic Rating – PT is at $1 152 – Potential of 71% + upside

Bull Thesis

Upward Surprises to Consider

1- EPS Miss Was Accounting Noise, Not Business Weakness and it Fried the Algos

- Reported EPS was hit, driven by a ~$15.9B one-time, non-cash tax charge.

- Excluding the charge, adjusted EPS was ~$7.25, above consensus.

- This will help them in increasing their depreciation and earnings over the long run.

2- Market Prices Only the Core Business

- META trades as a mature ad business, with valuation anchored to Facebook & Instagram cash flows.

- WhatsApp Business, Threads, AI monetization, Glasses, AR / VR and ecosystem potential synergy contribute little to current market pricing.

- Any incremental success from these segments represents potential upside not embedded in estimates.

3- AI Researchers Joined the Company for a Reason

- At Meta’s scale, even small AI-driven gains materially expand their revenue. Which we have seen with higher-than-expected revenue and DAU.

- META continues to attract top-tier AI researchers, strengthening its model and product velocity. There is a reason why they are joining beyond salary and compensation, knowing they are already paid well in their current positions.

- AI improvements directly enhance ad efficiency, user engagement, and monetization per user.

1- Execution Risk: Heavy AI & CapEx Spending Could Compress Margins

- META continues to guide toward elevated AI and infrastructure CapEx, pressuring near-term margins.

- If AI monetization ramps slower than expected, returns on investment may lag capital deployed.

- The market may penalize META if spending intensity remains high without clear revenue inflection.

2- Advertising Cyclicality & Macro Sensitivity

- META remains highly exposed to global advertising budgets, which are cyclical by nature.

- Economic slowdowns could lead to lower CPMs and ad demand volatility.

- Even strong engagement does not fully insulate revenue during broad ad market contractions.

3- Regulatory & Platform Risk Remains Structural

- META operates under ongoing regulatory scrutiny across privacy, data usage, and competition.

- Policy changes like some countries are limiting the age for social media, could lower the future revenue.

- There could be some retaliation and charges that the company would have to pay. Their reach is over 3 billion, making it a potential target.

Bear Thesis

Downward Surprises to Consider

Other Sources

Links for relevant YouTubers / Authors

1– Steven Fiorillo – Earnings Season is here

- The tax headline confused the market, the revenue is accerelating and the active users is growing.

- Margins are amazing, FCF margins went lower due to CAPEX, but they still get 30% net income margin +.

2– Future Investing – Top 4 stocks to BUY NOW for 2026

- This one-time tax charge did hit their EPS; however they did beat expectations. It sold off a bit too much.

- Users, engagement, revenue per users is increasing with AI.

- META is the cheapest of the mag 7 right now.

3– META Threads overtakes X in daily mobile users – Yahoo Finance

- 141.5 Daily Active Usuers vs 125 million Daily Active Users on X January 7th.

- The monetization of Threads – Whatsapp and other moonshots like AR / VR isn’t even fully materialized yet.