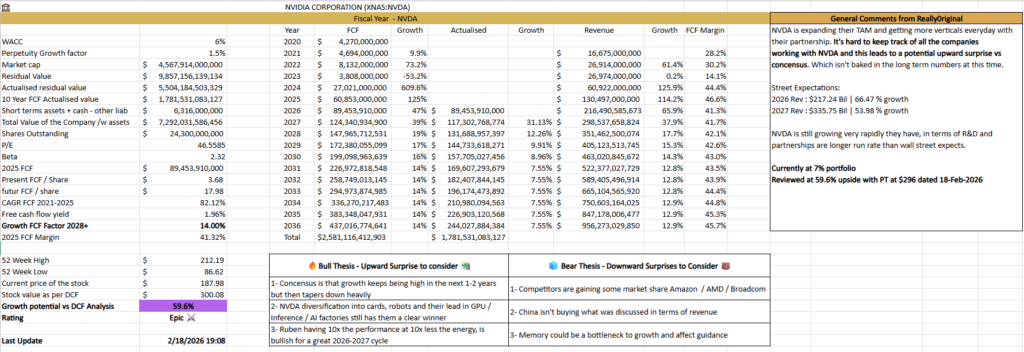

NVDA – Epic Rating – PT is at $300- Potential of 60% + upside

Bull Thesis

Upward Surprises to Consider

1- Concensus is high in growth rate, then it tapers down quickly

- Looking into the verticals and the businesses they are investing in, they are building their future once the buildup slows down.

- This includes parternships like Siemens (to make efficient AI factories, to improve supply chains).

- Full self driving, now available to other companies and we can expect that technology to be applied to humanoid robots and deliveries.

- Health sciences / Digital twins (AI simulations of the real world) and their pace of innovation is underestimated. Most recently Jensen mentioned a new chip will be unveiled at the next GTC (March 2026).

2- That diversification will be key for them in the future

- As they invest in startups and established players, they get deeper into the system with their AI software, we will see NVDA win even if the big Capex spend slows down a bit.

- The biggest difference in my analysis versus the concensus of Wall Street is that I expect the hyperscalers to by 40% FY 2027 and 17% FY 2028, as the biggest companies will want to slow down their growth of spend.

- However, that growth will continue on for many years with data centers updates, software and services paying off.

3- Vera Rubin sales will be better than expected

- Blackwell demand exceeded expectations, and supply execution was stronger than anticipated.

- Vera Rubin comes in when the AI race is heating up, making it a possibility that some hyperscalers may want to overspend to capture the future business. It also performs better than Blackwell with a stronger energy efficiency which is a key bottleneck.

1- Competitors are starting to gain traction

- Amazon: Trainium and Graviton have a $10 bil annualized revenue run rate as per Jassy’s comment. So roughly $2.5 bil to keep coherent with the quarterly outlook labelled below.

- AMD: Latest quarter in data center revenue was $5.4 bil. Lisa Su mentioned that there is just not enough compute to meet the demand right now.

- Broadcom: They have done $6.5 bil latest quarter on AI chips only. Expecting it to grow to the next quarter Q1 2026 at $8.2 bil.

2- China revenue remains a metric that is hard to put on a spreadsheet, for now

- Jensen mentioned that half of the AI engineers are in China, this market was still closed up until recently. Future revenue growth could face structural pressure as domestic players like Huawei are strongly supported by national policy.

- The 10-15% swing of revenue could be quite significant as China may decide to block NVDA chips, if they find better alternatives in the near term.

3- Memory could be a near term bottleneck

- This could affect guidance and also give the space for other competitors to gain a bit of market share, which would impact the future cash flows expected.

Bear Thesis

Downward Surprises to Consider

Final Comments

NVIDIA is a structural compounder and terminal value remains the key debate

We can see it with the partnerships, the high growth rates and the innovation at a pace we never

saw before.

NVDA will keep winning and we are still not realising the full extent of the potential payoff. Even if it’s a highly valued company at $4.6 trillion, the growth rates, the innovation and the technology is difficult to understand.

Which makes it a very interesting company to analyse, knowing that there could be big gap between what is priced in and the real value of this company.

This is not financial advice, and this is simply for information and entertainment purposes. Do your own due diligence on this and I am simply sharing my thoughts on this security.