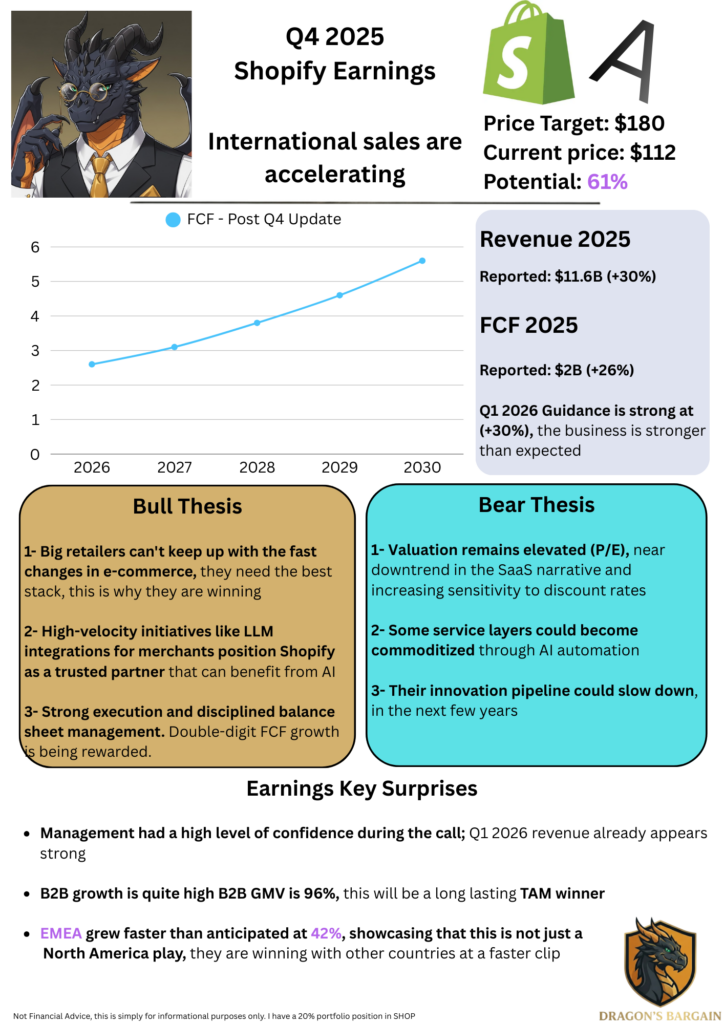

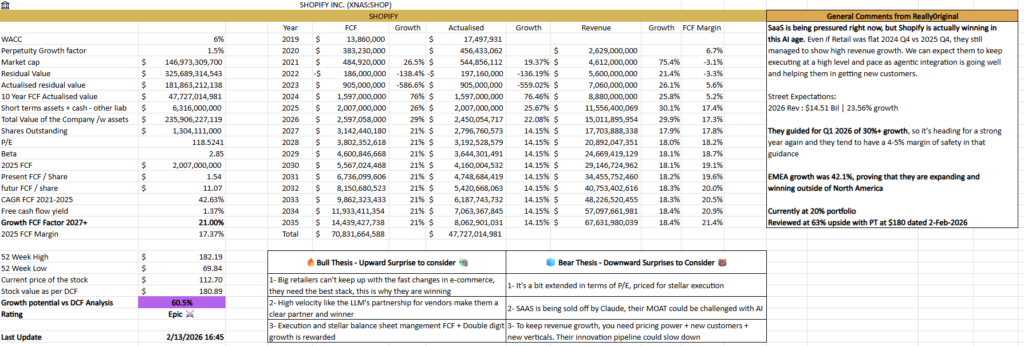

Shopify remains strong and I was surprised by the actual international growth which is quite Underappreciated

Shopify has been winning brands over the past few years, becoming the partner of choice when it comes to adapting to new trends and AI. More and more, we are seeing them outperform with their merchants. They are acquiring business from big brands that were previously in-house and moving them to the next step.

I remain very bullish on the name, knowing that they are moving forward in what I believe are the two most important TAMs needed for their business to grow.

- The B2B space is a great TAM for them to go after. Most of those B2B websites tend to be running on older technology. It takes time to get into the B2B space, but with the GMV growth and Shopify’s expertise, they will get there and win in the long run.

EMEA grew at a 42% clip, which is quite impressive. Even though they are market share gainers, they need to gain internationally to justify the growth they are building and they are making it, as we can see in the numbers.

The recent drop makes the business even more worthwhile to look at. I see a potential upside of 61% as per the DCF analysis

This is not financial advice, and this is simply for information and entertainment purposes. Do your own due diligence on this and I am simply sharing my thoughts on this security.